我们不再支持这个浏览器. Using a supported browser will provide a better experience.

请 更新浏览器.

2022年8月24日 拜登政府宣布 it would cancel up to $20,000 of federal student debt for certain borrowers. Borrowers with incomes less than $125,000元或250元,000 for joint filers are eligible for cancellation. Borrowers who received Pell grants at some point are eligible to have their debts cancelled up to $20,000, and all other borrowers are eligible to have $10,000年取消了.

We use administrative 追逐 banking and credit bureau data on 200,000 student debt holders to estimate how the benefits of this cancellation program might be distributed by household income and borrower 比赛 和种族.1

我们发现:

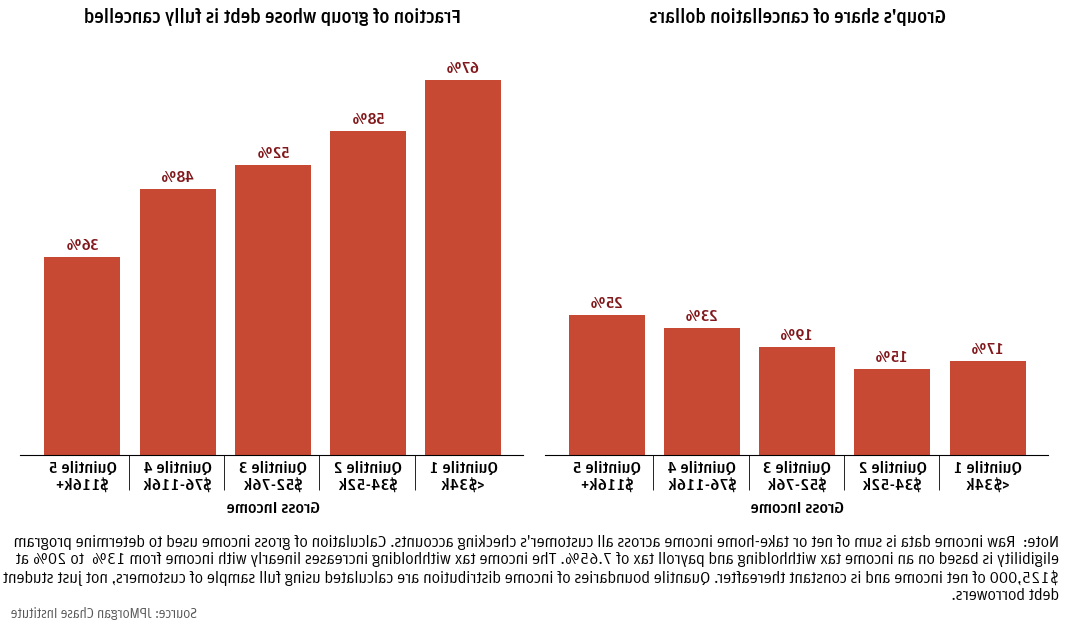

Figure 1: Higher income households receive slightly more cancellation dollars, but lower income households are more likely to have their debt fully cancelled.

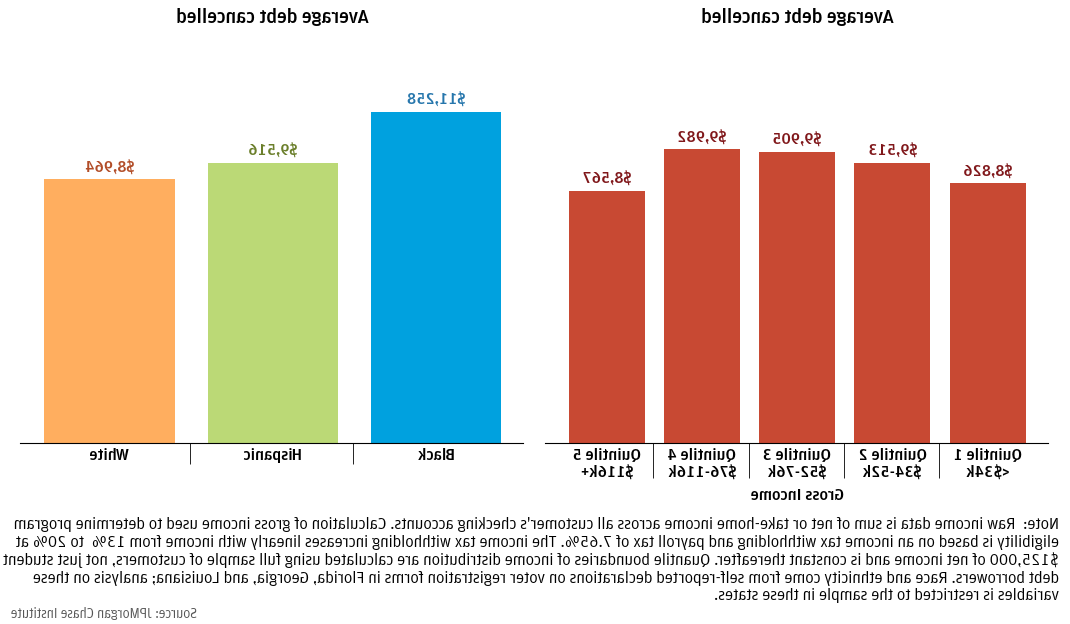

Figure 2: 平均债务被取消 among those receiving cancellation is between $9,000元及10元,在不同的收入范围内增加了000美元, but relatively higher for 黑色的 households.

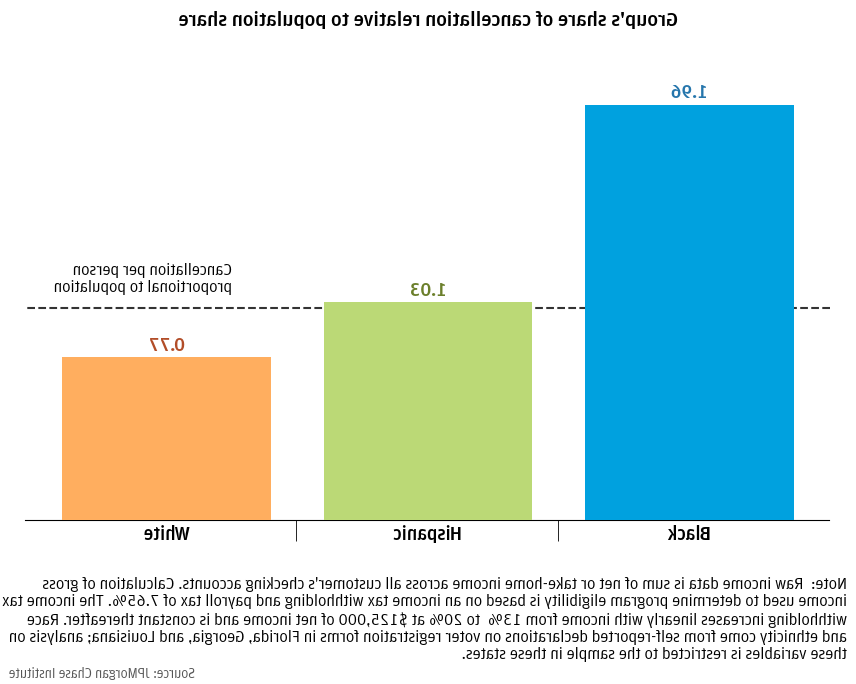

Figure 3: 黑色的 and 拉美裔 households receive more cancellation relative to their population share.

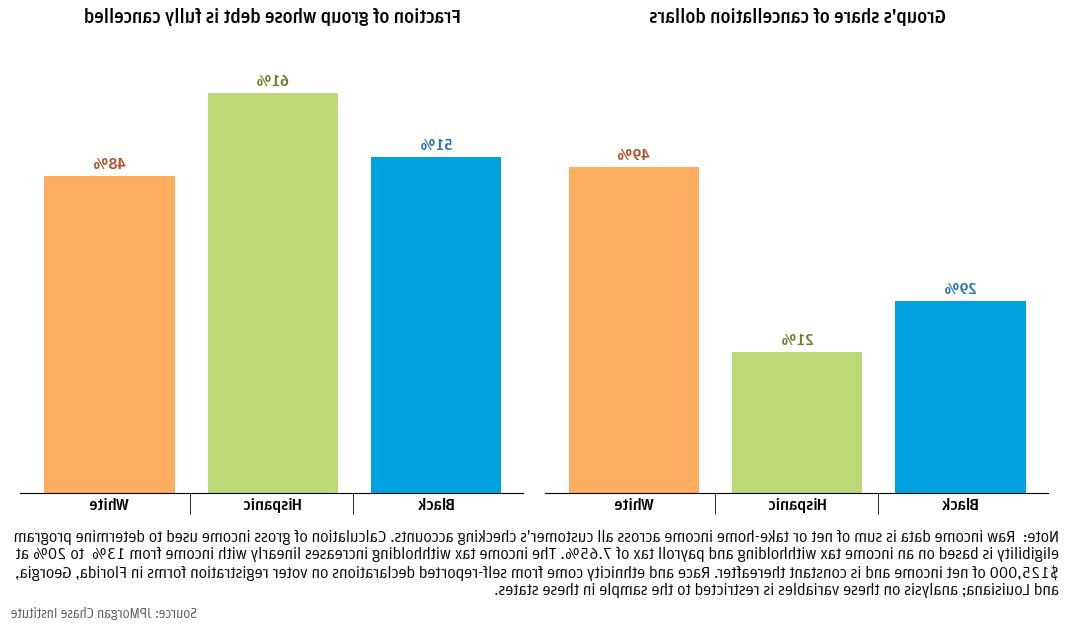

Figure 4: The distribution of cancellation dollars by 比赛 和种族 is proportional to the distribution of debt held by each group.

Cominole, M.纽约州里奇(Ritchie.S., & 库尼J. (2020). 2008/18 Baccalaureate and Beyond Longitudinal Study (B&B:08/18)数据文件文件 道理,2021 - 141年). U.S. 教育部. Washington, DC: National Center for Education Statistics, 研究所 of Education Sciences. 摘自8/24/2022 http://nces.ed.gov/pubsearch.

Farrell, Diana, Fiona Greig, and 丹尼尔米. 沙利文. 2020. “Student Loan Debt: Who is Paying it Down?12bet官方研究所. http://8ns6.deckblatt-bewerbung.net/corporate/institute/household-debt-student-loan-debt.

格雷格,菲奥娜和丹尼尔M. 沙利文. 2021. “Who benefits from student debt cancellation?12bet官方研究所. http://8ns6.deckblatt-bewerbung.net/institute/research/household-debt/who-benefits-from-student-debt-cancellation.

我们感谢我们的研究团队, 特别是伯纳德·何, for his hard work and contribution to this research. 另外, 我们感谢伊丽莎白·埃利斯, Kristine范教授, 安娜贝利Jouard, 斯蒂芬·哈林顿, Kate Finnerty and Clarke Wilson for their support. We are indebted to our internal partners and colleagues, who support delivery of our agenda in a myriad of ways, and acknowledge their contributions to each and all releases.

We are also grateful for the invaluable constructive feedback we received from external experts and partners. We are deeply grateful for their generosity of time, insight, and support. This research was possible because of the vital partnership, data, and knowledge from Experian.

We would like to acknowledge Jamie Dimon, CEO of 12bet官方 & Co., for his vision and leadership in establishing the 研究所 and enabling the ongoing research agenda. We remain deeply grateful to Peter Scher, 副主席, 德米特里Marantis, 企业责任主管, 希瑟Higginbottom, 研究主管 & 政策, and others across the firm for the resources and support to pioneer a new approach to contribute to global economic analysis and insight.

This material is a product of 12bet官方研究所 and is provided to you solely for general information purposes. Unless otherwise specifically stated, any views or opinions expressed herein are solely those of the authors listed and may differ from the views and opinions expressed by J.P. 摩根 Securities LLC (JPMS) 研究 Department or other departments or divisions of 12bet官方 & Co. 或者它的附属机构. This material is not a product of the 研究 Department of JPMS. Information has been obtained from sources believed to be reliable, but 12bet官方 & Co. 或者它的附属机构 and/or subsidiaries (collectively J.P. 摩根) do not warrant its completeness or accuracy. Opinions and estimates constitute our judgment as of the date of this material and are subject to change without notice. The data relied on for this report are based on past transactions and may not be indicative of future results. The opinion herein should not be construed as an individual recommendation for any particular client and is not intended as recommendations of particular securities, 金融工具, or strategies for a particular client. This material does not constitute a solicitation or offer in any jurisdiction where such a solicitation is unlawful.

12bet官方 & Co.'s website terms, privacy and security policies don't apply to the site or app you're about to visit. 请 review its website terms, privacy and security policies to see how they apply to you. 12bet官方 & Co. isn't responsible for (and doesn't provide) any products, services or content at this third-party site or app, except for products and services that explicitly carry the 12bet官方 & Co.