我们不再支持这个浏览器. 使用受支持的浏览器将提供更好的体验.

请 更新浏览器.

A central question for any government assistance program is how to reach the people who need help as quickly as possible while also making sure that those who receive help actually needed it?

研究表明,不需要文件的抵押贷款延期计划在很大程度上被房主所利用.

最近的12bet官方研究所 研究 在抵押贷款延期的背景下研究了这个问题.1 在新型冠状病毒肺炎大流行的早期, 冠状病毒援助, 救援, 和《12bet官网》为大多数房主提供了长达一年的担保2 如果他们在没有文件要求的情况下证明自己有与新冠病毒相关的困难,就可以获得付款减免. 使用行政抵押服务和支票账户数据, 我们几乎没有发现与该项目有关的道德风险的证据.

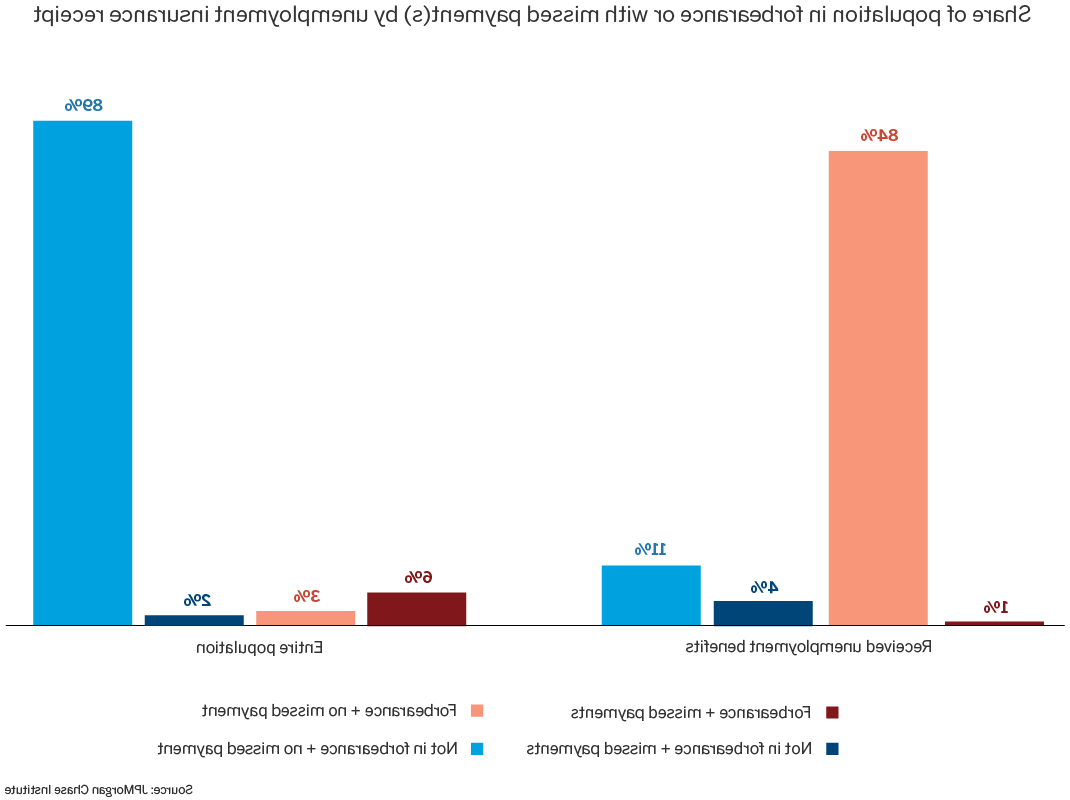

Borrowers using forbearance to miss mortgage payments had larger drops in income than other homeowners and experienced income changes similar to those who became delinquent without the protection of forbearance. 除了, borrowers in forbearance were more likely to have lost labor income and received unemployment benefits than borrowers not in forbearance. 事实上, 我们观察到的那些领取直接存入失业保险的人, 84 percent were in forbearance and continuing to make their mortgage payments and only 1 percent were in forbearance but missing mortgage payments. 换句话说, almost all of those who received UI and signed up for forbearance continued to make mortgage payments when they were able to.3 (图1)

Figure 1: Those who lost their jobs and were receiving unemployment insurance overwhelmingly opted into forbearance but did not use it.

与此形成鲜明对比的是, 经济大衰退时期的项目有严格的文件要求,但接受度很低.

大萧条时期, 旨在帮助陷入困境的房主的项目要求提供大量文件. 此后的研究表明,这些要求阻碍了许多此类项目的成功. The Hardest Hit Fund (HHF) was established in 2010 to offer mortgage payment assistance for unemployed or underemployed homeowners. 截至2016年底,只有29.2万名房主受益于HHF. The Home Affordable Unemployment Program (UP) was introduced in 2010 to provide assistance to unemployed homeowners who were unable to make their mortgage payments. 截至2016年底,只有46,485名房主参加了UP计划.4 类似的, 住房负担得起的修改计划(HAMP)等抵押贷款修改计划的使用率也很低. 从2009年3月到2010年6月,约有55%(近675人),000) of HAMP trial modifications were cancelled because homeowners could not provide the requisite income verification documentation.5 到2015年4月, more than one million homeowners had been denied a HAMP modification because they did not provide the financial and/or hardship verification documentation required to complete the evaluation of their request in a timely manner.6 最后, 研究表明,在此期间,与再融资计划相关的类似要求(e.g., 住房可负担再融资计划(Home Affordable Refinance Program)将贷款比例限制在50%以下. 因此,这些再融资项目对止赎率的影响不大.7

12bet官方银行研究所的数据也显示,几乎没有证据表明房主出现了战略性违约

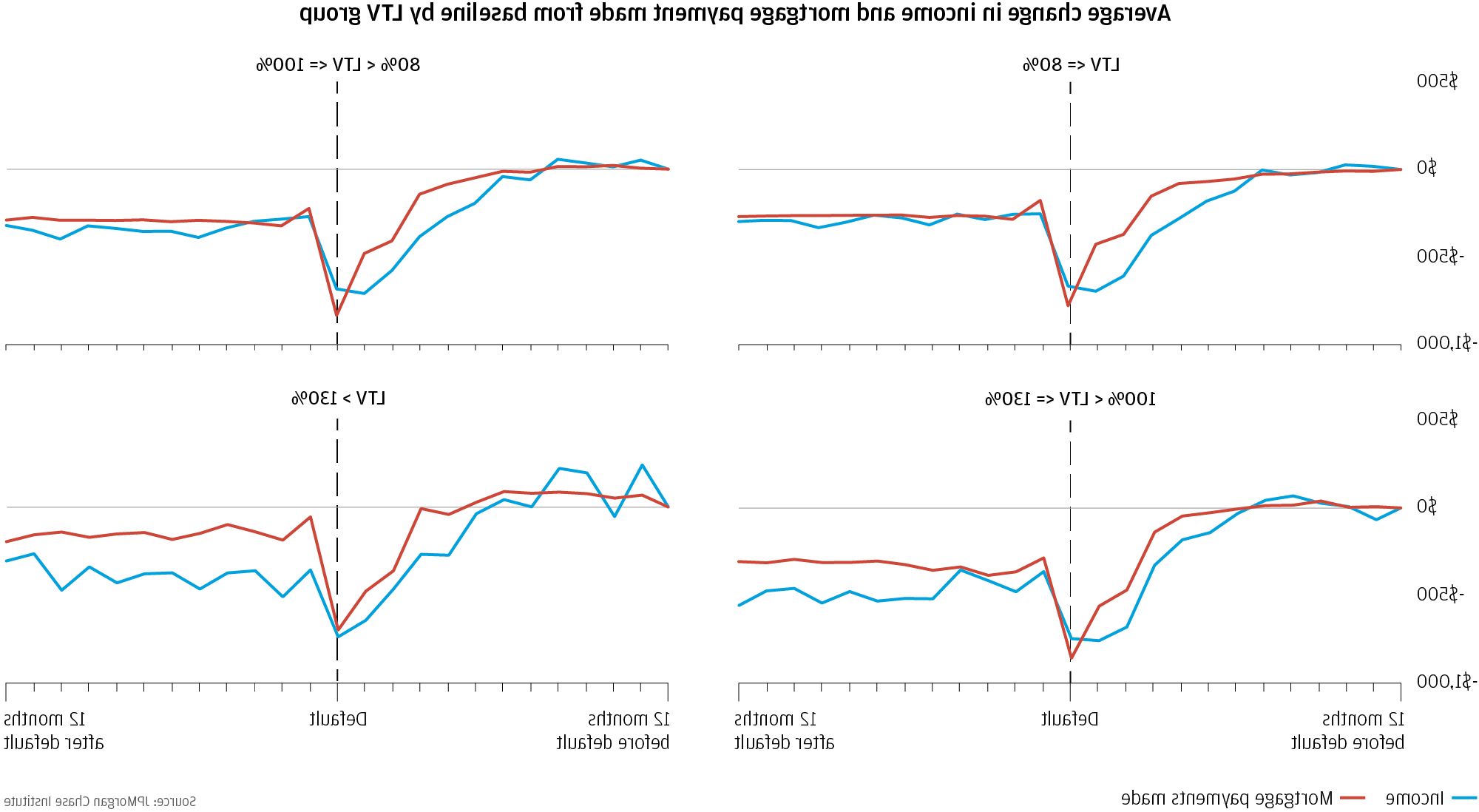

大萧条时期, many homeowners were underwater and policymakers were worried about strategic default—the risk that homeowner would walk away from their debt obligation once the mortgage exceeded the value of their home. 有证据表明,总的来说,房主并没有这样做. 使用抵押服务和存款账户数据,JPMC研究所 研究 对于拖欠抵押贷款的借款人来说, 违约紧随负收入冲击而来,无论他们的房屋净值水平如何. 即使房主深陷水中,情况也是如此.8 (图2)此结果与上面描述的简单类型的策略默认不一致. 加农和诺埃尔(2020), 使用JPMC研究所的数据, 将资不抵债的借款人与没有战略违约动机的群体进行比较:房屋净值为正的借款人. They find that only 3 percent of defaults are caused exclusively by negative equity and that adverse events are a necessary condition for 97 percent of mortgage defaults.9 This suggests that homeowners see their homes as more than a financial asset and place a high priority on being able to remain in their homes.

图2:违约对整个LTV分布的借款人产生负收入冲击, providing suggestive evidence against a simple model of strategic default where deeply underwater borrowers stop making mortgage payments only because they are underwater.

Renter assistance programs are fundamentally different from mortgage forbearance programs but may also see low take-up if documentation requirements are too onerous

该研究所 研究 与抵押贷款持有者相比, renters were on weaker financial footing prior to the pandemic and experienced greater job losses and labor income declines during the pandemic. 此外, 尽管失业保险和经济福利检查的慷慨扩大增加了许多租房者的总收入, 超过五分之一的人的总收入下降了10%以上. 最后, renters entered the pandemic with much lower levels of savings and their relative position did not improve meaningfully during the pandemic despite government stimulus programs as they depleted more of the stimulus-generated additional savings by the end of the year than mortgage holders. 重要的是, these results likely represent a “best case scenario” for renters since 研究所 data capture a sample of renters that skew higher in income. An analysis that includes more low-income renters—especially those that are underbanked or already struggling with housing payments—would likely show worse financial outcomes for renters.10 这些结果表明,租房者需要某种形式的租房援助.

而租赁援助计划已经在一些特定的地方存在, the main form of rental assistance during the pandemic arrived in December 2020 with the Consolidated Appropriations Act of 2021, 为州和地方政府建立了250亿美元的联邦紧急租赁援助计划. 为了申请这个项目, 租房者被要求填写表格并上传证明失业或收入损失的文件, 无家可归或住房不稳定的风险, 收入不超过地区收入中位数(AMI)的80%.11 如此广泛的要求可能, 类似于大衰退时期的住房援助计划, 导致许多租房者无法获得援助,因为他们无法证明自己的需要.g., 他们需要协助填写申请表, 他们的收入很难记录下来, 等.). It is worth acknowledging that rental assistance is fundamentally different from mortgage forbearance: rental assistance provides a transfer of money to renters, 而忍耐是债务义务的延期. 另外, 当涉及到住房支付时,租房者可能会表现出与房主不同的行为. 也就是说, the 研究 around moral hazard and uptake for mortgage forbearance and Great Recession-era housing programs is still instructive. 像这样, policymakers may consider revisiting whether the right balance between accessibility and fraud prevention has been found in rental assistance programs.